European Commission takes next step towards CSRD implementation

The European Commission has taken an important next step by revising the European Sustainability Reporting Standards (ESRS) initially drafted by the European Financial Reporting Advisory Group (EFRAG). Where are we in the governance process? And what are the revisions introduced by the European Commission to align the ESRS with the Corporate Sustainability Reporting Directive (CSRD)?

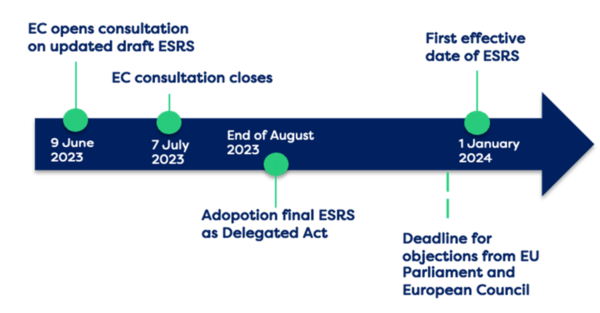

The implementation process of the ESRS has reached a significant milestone! The revised ESRS is currently undergoing a public consultation and will likely be adopted by European Commission as a delegated act by end of August. If there is no objection from the European Parliament and the European Council, the first effective date of the ESRS will be January 1st, 2024.

In November 2022, the EFRAG completed the final draft of the ESRS. These standards form the bedrock of the Corporate Sustainability Reporting Directive (CSRD), which mandates that companies disclose non-financial or sustainability data alongside their financial information. The CSRD is set to come into effect on the 1st of January 2024. To ensure companies have enough time to prepare for the CSRD, the ESRS need to be finalized and accepted at least 4 months prior to this date.

On the 7th of July the consultation priod ended and the European Commission received 604 reviews. Of those, more than 50% were from companies and business associations and 13% were based in the Netherlands. At Schuttelaar & Partners, we are now eagerly awaiting the acceptance and publication of the final delegated act, so we can further solidify our advice.

In our advisory role, we keep track of the revisions that were made by the European Commission to the original EFRAG standards. We have seen that the changes were mostly focussed on alleviating reporting pressure for companies. The European Commission implemented three significant changes:

1. Decreasing the obligatory nature of the standards and some disclosure requirements

In the EFRAG standards ESRS 2; general disclosure requirements, ESRS E1; climate change, and ESRS S1; own workforce, were mandatory regardless of the double materiality analysis. However, in the delegated act only ESRS 2 remains mandatory. Moreover, certain disclosure requirements have been modified, to scale back the mandatory nature of the standards, for example "shall" has been changed to "may’’, "if applicable" has been added, and some mandatory disclosure requirements have been completely removed from the text. Such as in ESRS 4; biodiversity and ecosystem, where in the EFRAG version, doing a life cycle assessment was a mandatory requirement, and now a company ‘may’ execute one.

2. Streamlining the topical standards

The topical standards, focusing on specific material topics in the E-S-G domains, have undergone simplification. Previously, reporting guidelines for policies, targets, actions, and metrics were discussed separately in each topical standard. However, the ESRS 2, known as General Disclosures, now summarizes these reporting aspects for each topical standard. This approach reduces complexity, provides clarity, and establishes a cohesive structure for CSRD reports aligned with the ESRS. Also, we have noticed that examples are left out of the text and that sentences are simplified. All in all, the ESRS are reduced from 12 documents of around 40 pages to one document of 247 pages.

3. Gradual roll-out

For various disclosures, specifically for the value chain and financial impact, are not immediately available mandatory for (all) companies.

These revisions, though sometimes small, have a significant impact on consultants, companies, and accountants who are preparing for the CSRD. It is hoped that the standards will be adopted promptly so that everyone can begin strategizing, implementing, and acting in alignment with this new sustainability framework.